Performance & Portfolio

We ended the year with a net portfolio value of S$389 billion2. Marking our unlisted portfolio to market would provide S$31 billion of value uplift and brings our net portfolio value to S$420 billion3.

S$389b

Net portfolio value

Up S$166 billion over the last decade

(as at 31 March)

Net Portfolio Value (S$b)

Temasek Net Portfolio Value since Inception

- Market value

- Shareholder equity

- Shareholder equity excluding mark to market movement4

1 Incorporation of Temasek on 25 June 1974.

2 Financial year 75 began on 25 June 1974 and ended 31 December 1975.

3 Financial year-end was changed from 31 December before 1993 to 31 March from 1994 onwards.

4 From the financial year ended 31 March 2006, the accounting standards require sub-20% investments to be marked to market.

Our portfolio comprises both listed and unlisted investments.

Our net portfolio value of S$389 billion is based on valuing our listed investments at share prices as of the last trading day of our financial year and our unlisted investments at book value less impairment. Book value refers to Temasek’s cost of investment plus our share of the investee company’s profits or losses, changes in other equity reserves, minus write down (if any).

Over the last decade, our unlisted portfolio generated returns of 9% per annum, delivering higher returns than our listed portfolio.

Marking our unlisted portfolio to market, based on market approaches such as investee company’s recent funding round, market multiples of comparable public companies, and/or income approach such as the discounted cash flow model, would provide S$31 billion of value uplift, which is approximately 15% of our unlisted portfolio as at 31 March 2024.

S$26b

Invested during the year

Invested S$328 billion over the last decade

(for year ended 31 March)

Investments & Divestments (S$b)

- Investments

- Divestments

6%

10-year return to shareholder

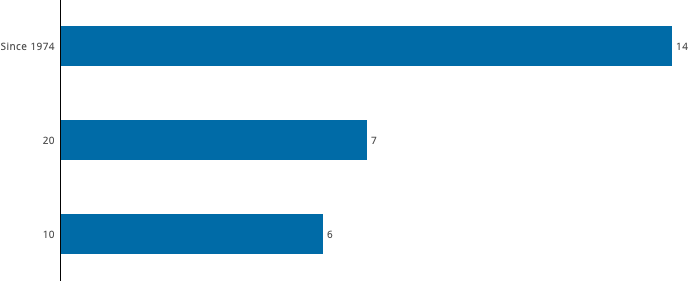

Total shareholder return of 14% since inception

(as at 31 March 2024)

S$ Total Shareholder Return (%)

Period in years1

Period in years1

1 Total Shareholder Return in US$ terms was 5%, 8%, and 15% for 10, 20-year, and since inception periods respectively, based on historical foreign exchange rates.

Total Shareholder Return (TSR) is a compounded and annualised measure, which includes dividends paid to our shareholder and excludes investments made by our shareholder in Temasek’s shares. Our TSR over different time periods is a snapshot of our performance, with the longer time periods being more representative of our performance as a long-term investor.

As at 31 March 2024, our Singapore dollar4 10-year TSR was 6% and three-year TSR was 0.68%.

Our 20-year TSR was 7%, versus the Singapore 20-year annualised core inflation5 of 1.9%.

7%

20-year return to shareholder

One-year returns of -9% to 25% during the last decade

(as at 31 March)

Rolling S$ Total Shareholder Return (%)

- One-year

- 10-year

- 20-year

S$9b

Dividend income

Average annual dividend income of S$9 billion over the last decade

(for year ended 31 March)

Dividend Income (S$b)

Anchored in Asia, our S$389 billion6 portfolio has 64% underlying exposure to developed economies.

(as at 31 March)

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Singapore

|

53 | 54 | 54 | 49 | 52 | 55 | 54 | 60 | 60 | 57 |

|---|---|---|---|---|---|---|---|---|---|---|

|

China

|

13 | 15 | 15 | 21 | 23 | 20 | 20 | 19 | 20 | 21 |

|

India

|

5 | 3 | 3 | 3 | 2 | 2 | 2 | 3 | 2 | 2 |

|

Asia Pacific (ex Singapore, China & India)

|

2 | 2 | 2 | 2 | 3 | 4 | 5 | 4 | 5 | 5 |

|

Americas

|

17 | 16 | 17 | 15 | 12 | 11 | 12 | 8 | 7 | 7 |

|

Europe, Middle East & Africa

|

10 | 10 | 9 | 10 | 8 | 8 | 7 | 6 | 6 | 8 |

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Singapore

|

27 | 28 | 27 | 24 | 24 | 26 | 27 | 29 | 29 | 28 |

|---|---|---|---|---|---|---|---|---|---|---|

|

China

|

19 | 22 | 22 | 27 | 29 | 26 | 26 | 25 | 25 | 27 |

|

India

|

7 | 6 | 6 | 5 | 4 | 5 | 4 | 5 | 5 | 5 |

|

Asia Pacific (ex Singapore, China & India)

|

12 | 11 | 12 | 12 | 14 | 15 | 18 | 17 | 19 | 19 |

|

Americas

|

22 | 21 | 21 | 20 | 18 | 16 | 14 | 14 | 12 | 11 |

|

Europe, Middle East & Africa

|

13 | 12 | 12 | 12 | 11 | 12 | 11 | 10 | 10 | 10 |

1 Distribution based on underlying assets.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Transportation & Industrials2

|

22 | 23 | 22 | 19 | 18 | 19 | 19 | 20 | 21 | 22 |

|---|---|---|---|---|---|---|---|---|---|---|

|

Financial Services

|

21 | 21 | 23 | 24 | 23 | 25 | 26 | 25 | 23 | 28 |

|

Telecommunications, Media & Technology

|

18 | 17 | 18 | 21 | 21 | 20 | 21 | 23 | 25 | 24 |

|

Consumer & Real Estate

|

15 | 16 | 15 | 14 | 17 | 17 | 16 | 17 | 17 | 15 |

|

Life Sciences & Agri-Food

|

9 | 9 | 9 | 10 | 8 | 7 | 6 | 4 | 4 | 3 |

|

Multi-Sector Funds

|

9 | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 7 | 5 |

|

Others (including Credit)

|

6 | 6 | 5 | 4 | 5 | 4 | 4 | 3 | 3 | 3 |

1 Distribution based on underlying assets.

2 The Transportation & Industrials sector includes investments in Energy & Resources.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Liquid & sub-20% listed assets1

|

29 | 27 | 28 | 38 | 37 | 36 | 36 | 33 | 31 | 34 |

|---|---|---|---|---|---|---|---|---|---|---|

|

Listed large blocs (≥ 20% and < 50% share)

|

9 | 9 | 8 | 7 | 5 | 10 | 10 | 9 | 10 | 12 |

|

Listed large blocs (≥ 50% share)

|

10 | 11 | 12 | 10 | 10 | 12 | 15 | 18 | 20 | 21 |

|

Unlisted assets

|

52 | 53 | 52 | 45 | 48 | 42 | 39 | 40 | 39 | 33 |

1 Mainly cash and cash equivalents, and sub-20% listed assets.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Singapore dollars

|

55 | 54 | 49 | 50 | 57 | 63 | 53 | 60 | 58 | 58 |

|---|---|---|---|---|---|---|---|---|---|---|

|

US dollars

|

30 | 30 | 34 | 31 | 26 | 21 | 24 | 19 | 19 | 14 |

|

Hong Kong dollars

|

5 | 7 | 7 | 11 | 11 | 10 | 12 | 12 | 13 | 15 |

|

Indian rupees

|

4 | 3 | 3 | 2 | 2 | 2 | 2 | 2 | 2 | 2 |

|

Euros

|

2 | 02 | 1 | 1 | 02 | 02 | 1 | 02 | 02 | 1 |

|

Others

|

4 | 6 | 6 | 5 | 4 | 4 | 8 | 7 | 8 | 10 |

1 Distribution based on currency of denomination.

2 Less than 1%.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Sustainable Living

|

121 | 5 | 2 | 1 | 1 | 02 | 02 | 02 | 02 | * |

|---|---|---|---|---|---|---|---|---|---|---|

|

Digitisation

|

11 | 10 | 11 | 9 | 7 | 6 | 3 | 3 | 2 | * |

|

Future of Consumption

|

10 | 11 | 11 | 14 | 11 | 9 | 10 | 8 | 8 | * |

|

Longer Lifespans

|

6 | 5 | 6 | 8 | 6 | 5 | 6 | 3 | 3 | * |

|

Others

|

61 | 69 | 70 | 68 | 75 | 80 | 81 | 86 | 87 | * |

1 The increase in our Sustainable Living exposure is mainly due to a reclassification of selected portfolio companies as at 31 March 2024, to better reflect their alignment with the trend.

2 Less than 1%.

* Information not measured in previous years. We have been aligning our portfolio to structural trends since 2016.

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | |

|

Technology

|

10 | 10 | 11 | 13 | 12 | 8 | 8 | 6 | 6 | 5 |

|---|---|---|---|---|---|---|---|---|---|---|

|

Non-Bank Financial Services

|

7 | 7 | 8 | 9 | 7 | 6 | 5 | 4 | 3 | 4 |

|

Life Sciences

|

6 | 6 | 6 | 8 | 6 | 5 | 5 | 4 | 4 | 3 |

|

Consumer

|

5 | 5 | 5 | 5 | 7 | 7 | 7 | 7 | 7 | 6 |

|

Agri-Food

|

3 | 3 | 3 | 2 | 2 | 2 | 1 | 01 | 01 | 01 |

|

Media

|

1 | 1 | 01 | 01 | 01 | 01 | 01 | 01 | 01 | 01 |

|

Others

|

68 | 68 | 67 | 63 | 66 | 72 | 74 | 79 | 80 | 82 |

1 Less than 1%.

Our investments are driven by our views of the trends shaping societies.

Since our incorporation in 1974, Temasek has transformed from a Singapore holding company into a global investment company. In the 2000s, we stepped out and grew with an emerging Asia. In 2010, we embarked on our strategy to be a global investor by the end of 2020, and expanded beyond investing in emerging markets and Asia, to developed markets in the US and Europe.

In 2019, Temasek developed our T2030 strategy — our 10-year roadmap to guide our strategic planning, capability building, and institutional development initiatives for this decade. As part of our T2030 strategy, we focus on constructing a resilient and forward-looking portfolio — one which is able to withstand exogenous shocks and perform through market cycles, while at the same time capitalising on growth opportunities with the potential for sustainable returns above our risk-adjusted cost of capital over the long term.

Portfolio Composition

Structural Trends

To guide our construction of a portfolio that is resilient to shocks and relevant for the future, our investment activities are aligned to four structural trends.

Digitisation and Sustainable Living are megatrends with a pervasive impact across all sectors and on the business models of incumbent and emerging businesses. Future of Consumption and Longer Lifespans reflect structural shifts in consumption patterns and growing needs arising from population growth and longer expected lifespans. These trends are interconnected, transcend sectors and countries, and persist through economic cycles.

We continue to align our portfolio with such trends. We invest in companies that directly enable, drive, and benefit from these trends.

In addition, we deploy capital to catalyse solutions that can enable companies to transition to a more sustainable future, tap on opportunities to invest in future growth sectors and business models, and encourage enterprises to transform through efforts in innovation.

We set aside a portion of our investment capital to back innovations and disruptive technologies at pre-commercialisation stages. We are cognisant of the risks and challenges these early-stage companies face and accept the binary risks that come with investing in them.

Listed and Unlisted

Our portfolio comprises both listed and unlisted assets, including our investments in funds. The unlisted portfolio has grown steadily over the years as we invested in attractive opportunities in the private markets and benefitted from the increase in the value of our unlisted assets.

As at 31 March 2024, 48% of our portfolio was in liquid7 and listed assets, and 52% was in unlisted assets and funds.

We value our unlisted investments at book value less impairment8. Our unlisted portfolio, including our private equity co-investments and investments in private equity funds, generated returns of 9% per annum over the last decade and more than 10% per annum over the last two decades, delivering higher returns than our listed portfolio.

Marking our unlisted portfolio to market9 would provide S$31 billion of value uplift which is approximately 15% of our unlisted portfolio as at 31 March 2024.

(as at 31 March 2024)

Unlisted Portfolio (%)

- Singapore Portfolio Companies1

- Asset Management Businesses

- Private Equity and Credit Funds

- Other Private Companies (Including Early Stage)

1 Includes only key portfolio companies headquartered in Singapore.

Our unlisted portfolio is well diversified across geographies and sectors.

Unlisted Singapore companies include mature companies such as Mapletree, PSA, and SP Group.

Our asset management businesses include Seviora Holdings10, Pavilion Capital, and Vertex Holdings. Our asset management businesses manage around S$83 billion in assets, which include third-party capital as well as our own capital.

Investments in private equity and credit funds have enabled us to gain deeper insights into new markets and sub-sectors of specialisation while providing co-investment opportunities.

The rest of our unlisted portfolio comprises direct investments in private companies. Our investments include Ant Group, AS Watson, Ceva Santé Animale, Element Materials Technology, Manipal Health Enterprises, Mastronardi, Schneider Electric India, and Topsoe.

Our unlisted portfolio offers us liquidity through divestments; steady dividends from mature companies; and distributions from the high-quality portfolio of funds we have built up over the years. The funds are well diversified across geographies, sectors, and vintages. We also achieve liquidity from our unlisted portfolio through public listings. For example, DoorDash, Gracell Biotechnologies, Intapp, Medanta, PB Fintech, and Zomato have listed in the past five years.

Early-Stage Investments

Our focus as an investment company is to invest in innovation and growth. This includes investing in early-stage companies to identify potential winners early; to keep abreast of the latest technologies and innovations; and to drive portfolio development efforts. We also engage closely with portfolio companies on their efforts to assess potential disruption risks and to identify transformation opportunities arising from these new technologies.

We are cognisant of the risks and challenges these early-stage companies face and accept the binary risks that come with investing in them. However, some of these companies also have the potential to achieve significant growth over time and deliver outsized returns.

We manage our early-stage risk by appropriate sizing and diversification. We typically invest smaller amounts at the time of initial investment, with a view to increasing our stake if the company demonstrates successful de-risking. In addition, we cap our exposure to this segment to 6% of our overall portfolio as part of our risk management framework. Currently, our early-stage investments account for under 6% of our total portfolio, with about half through direct investments and the rest through venture capital funds.

Integrating ESG Across Our Investments

We apply an Environmental, Social, and Governance (ESG) framework across our entire investment process. This includes investment due diligence to ensure that the opportunities we consider align with our objectives for sustainability and good governance. Post-investment, we engage investee companies to advance sustainability practices, including strengthening climate targets and transition plans, promoting inclusive workplaces as well as workplace health and safety, and fostering good governance.

Investment Framework and Risk-Adjusted Cost of Capital

Our investment discipline is centred around intrinsic value and our risk-return framework. This framework forms the basis of our investment decisions, capital allocation, performance measurement, and incentive system.

Our risk-adjusted cost of capital (RACOC) framework compares the relative attractiveness between investment opportunities. For each investment, we conduct a bottom-up intrinsic value analysis, with expected returns evaluated against a RACOC that we derive using the capital asset pricing model.

Each investment’s RACOC takes into account country risk, industry risk, and capital structure. Investments in riskier sectors or markets will have higher costs of capital. We reflect additional risk by adding to the RACOC an illiquidity risk premium for unlisted investments and a venture risk premium for early-stage investments.

We assess our performance by measuring our TSR against our overall RACOC, which is the weighted average RACOC across all our individual investments.

(as at 31 March 2024)

S$ Total Shareholder Return Relative to Risk-Adjusted Cost of Capital (%)

Period in years

- S$ Total Shareholder Return by Market Value1

- Risk-Adjusted Cost of Capital 2

- S$ Total Shareholder Return by Shareholder Equity3

1 TSR by market value takes into account changes in the market value of our portfolio, dividends we paid, and nets off any new investments made by our shareholder in Temasek’s shares.

2 Our risk-adjusted cost of capital accounts for different risks faced by our investments, and is derived using a capital asset pricing model. The risk-adjusted cost of capital is built bottom-up, and aggregated across all our investments.

3 TSR by shareholder equity takes into account the underlying profitability of our portfolio companies, realised returns from our investment activities, dividends we paid, and nets off any new investments made by our shareholder in Temasek’s shares.

(as at 31 March 2024)

S$ Total Shareholder Return Relative to Market Indices1 (%)

Period in years

- S$ Total Shareholder Return by Market Value

- FTSE STI2

- MSCI AC Asia ex-Japan3

- MSCI ACWI4

1 Temasek’s mandate is to deliver sustainable returns over the long term. These market indices are broad indices, including a wide range of stocks across different countries and industry sectors. The allocations of the indices across sectors and countries are typically based on the market capitalisation of listed stocks, and it is more commonly used for passive investing through Exchange-Traded Funds (commonly known as ETFs). Temasek’s portfolio composition is very different from these indices, especially as Temasek’s portfolio includes a proportion of unlisted assets. However, market indices provide useful broad reference points as to how the overall market had moved over time. Temasek has set out our performance against various indices, where there is a complete dataset available, to assist those interested in such comparisons.

2 The FTSE STI Index measures the performance of the top 30 companies listed on the Singapore Exchange.

3 The MSCI AC Asia ex-Japan Index measures the performance of large to mid-sized companies in Asia, excluding Japan.

4 The MSCI ACWI Index measures the performance of large to mid-sized companies in the developed and emerging markets.

We increased our internal carbon price from US$50 per tonne of carbon dioxide equivalent (tCO2e)11 in the financial year ended 31 March 2024 to US$65 per tCO2e starting from 1 April 2024. Our internal carbon price is applied to each investment to better assess the potential climate impact, thereby enabling a greater focus on the long-term climate resilience of our portfolio. We expect to progressively increase this to US$100 per tCO2e by 2030.

Investment Engagement and Stewardship

Against the challenges and uncertainties in our macro environment, companies have to be ever more agile and laser-focused on the development and execution of their strategies, in order to meet the expectations of their shareholders and other stakeholders.

As an investor and owner seeking to achieve sustainable long-term returns from our portfolio, Temasek stays committed to working with our portfolio companies, their boards, and leadership, to ensure a close alignment between strategy and performance, and returns and rewards. We seek to add value to our investee companies — where appropriate, we work together with these companies to enhance value through partnerships, innovation, growth strategies, and transformational possibilities.

As an engaged shareholder, we proactively promote good governance, ethical business practices, and compliance with applicable laws. We set clear expectations and exercise our rights through voting at shareholder meetings. We view voting and engagement as key levers that are essential to long-term value creation and have formed a dedicated Investment Stewardship function to augment that effort.

Amidst a bifurcated global economy, we took a cautious investment stance while staying guided by long-term structural trends.

We invested S$26 billion and divested S$33 billion in the financial year ended 31 March 2024, with a net divestment of S$7 billion. Our cautious investment stance was driven by expectations of a US recession until the Federal Reserve pivoted from its tight monetary policy in the last quarter of 2023, as well as the slower than expected pace of post-COVID recovery in China. Our divestments included the significant redemption of capital by Singapore Airlines and Pavilion Energy respectively.

Despite the market uncertainties, we believe that there are opportunities to be seized. The US remains the leading destination for our capital and we also stepped up our investment activities in Europe, India, and Japan.

Consistent with past years, we continued to deploy capital into opportunities aligned with the four structural trends and our sustainability objectives. We de-risked certain positions and realised gains from earlier investments. This will allow us to recycle our capital, and to take advantage of market dislocations and unique investment opportunities, as and when they arise.

Investing Across Key Sectors and Geographies

We made significant investments in consumer, financial services, healthcare, and technology sectors.

In India, we strengthened our healthcare and financial services portfolio with investments in Manipal Health Enterprises, a hospital chain; Niva Bupa, a health insurance company; and follow-on investments in Axis Bank, HDFC Bank, and ICICI Bank. We continued our support for emerging champions by investing in Atomberg Technologies, a consumer electricals company, and Skyroot, a space tech company which specialises in space launches for small satellites.

In North America, we invested in Authentic Brands Group, a brand licensing and development company with a portfolio of over 50 global brands; Microsoft, a software and cloud infrastructure company; and Twin Health, a digital therapeutics company focused on reversing chronic metabolic diseases. We re-invested in entertainment, sports, and media agency Creative Artists Agency, as part of its acquisition by Artémis. The investment furthers our partnership with the company and its new owner in its next phase of growth. We also made follow-on investments in iCapital Network, a financial technology company that provides access to alternative investments, and MSCI, a provider of indexes and investment solutions.

In Europe, we invested in ASML, a Netherlands-based semiconductor capital equipment provider in the lithography sector, and H2 Green Steel, a Sweden-based company that aims to accelerate the decarbonisation of the steel industry using green hydrogen.

In China, we invested in companies underpinned by structural trends like Digitisation and Longer Lifespans. For example, we invested in Bambu Lab, a consumer tech company focused on 3D printers, and Viva Biotech, a one-stop drug research and development platform.

Southeast Asia continued to offer investment opportunities aligned with the structural trend of Future of Consumption. During the year, we increased our investment in Sea Limited, a global consumer Internet company based in Singapore.

In line with growing digitisation, the availability of Large Language Models has accelerated the experimentation and adoption of generative Artificial Intelligence (AI) across sectors and geographies. We are deepening our understanding of the enablers, adopters, and beneficiaries of generative AI. To this end, we have invested in companies that enable the effective implementation of AI on a large scale. These included companies involved in advanced semiconductor technologies and data centre infrastructure. In addition, several of our portfolio companies are actively expanding their data centre business, such as Keppel Data Centres, Mapletree, Singtel, and ST Telemedia. We have made investments in companies that specialise in the development of AI-enabled applications, which contribute to enhancing business productivity. Our subsidiary, Aicadium, has been working with selected portfolio companies on value-creation AI use cases to uplift returns. Amidst the momentum and optimism for generative AI, we maintain a disciplined and cautious approach to investing in AI-related businesses.

Investing to Drive Sustainable and Inclusive Growth

We have been stepping up investments in companies that enable the transition towards a more sustainable future. Such efforts are aligned with the Sustainable Living trend, a megatrend that has pervasive impact across all sectors and on business models.

Over the year, we invested in companies developing innovative electrification solutions across the battery value chain. In the area of battery storage, we co-led with Decarbonization Partners a funding round for Ascend Elements, a US-based company that produces engineered battery materials from upcycled waste and scrap batteries. In the area of electric mobility, we invested in Electric Vehicle (EV) companies in India and China, with new investments in Mahindra Electric Automobile, an India-based company that manufactures four-wheeler passenger EVs, and BYD, a pioneer EV and battery manufacturer in China. We also made a follow-on investment in Ola Electric, an India-based electric two-wheeler manufacturer.

We invested in companies across the hydrogen value chain which are creating promising clean energy solutions. Over the year, we invested in US-based companies that manufacture, deliver, and commission electrolysers for critical industries to produce low-cost green hydrogen. For example, we made a new investment in Electric Hydrogen and a follow-on investment in Verdagy.

We continued to invest in funds and companies that aim to generate a positive impact for underserved communities while achieving sustainable returns over the long term. Over the year, we committed to funds that aim to enable climate mitigation in underserved communities. These included LeapFrog’s Climate Fund, which addresses climate change in Africa and emerging markets in Asia, and ABC Impact’s Fund II, which focuses on achieving positive social or environmental outcomes in Asia.

Find out more about how we embed sustainability in our investments

- Financials for the companies are based on their respective annual filings.

- Market relevant information is sourced from Bloomberg, Stock Exchanges, and public filings by companies.

Market Capitalisation = Market value as at 31 March 2024 and 31 March 2023

Shareholder Equity = Shareholder equity reported by the respective companies based on their annual filings

| Logo | Name |

Shareholding2 (%)

as at 31 March 2024 |

Currency |

Market Capitalisation or Shareholder Equity1 |

Sector | Headquarters | |

|---|---|---|---|---|---|---|---|

2024 |

2023 |

||||||

|

|

Adyen N.V. | 6 | EUR’m | 48,681 | 45,237 | Financial Services | Netherlands |

|

|

AIA Group Limited | 3 | HKD’m | 593,481 | 964,512 | Financial Services | Hong Kong SAR |

|

|

Alibaba Group Holding Limited | <1 | USD’m | 176,097 | 261,836 | Telecommunications, Media & Technology | China |

|

|

AS Watson Holdings Limited3 | 25 | HKD’m | 37,176 | 33,555 | Consumer & Real Estate | Hong Kong SAR |

|

|

Bayer Aktiengesellschaft | 3 | EUR’m | 27,901 | 57,541* | Life Sciences & Agri-Food | Germany |

|

|

BlackRock, Inc. | 3 | USD’m | 124,021 | 100,304 | Financial Services | US |

|

|

CapitaLand Group Pte. Ltd. | 100# | SGD’m | 13,404 | 14,444 | Consumer & Real Estate | Singapore |

|

|

Celltrion, Inc. | 3 | KRW’b | 39,550 | 21,348 | Life Sciences & Agri-Food | South Korea |

|

|

DBS Group Holdings Ltd | 29 | SGD’m | 93,152 | 85,102 | Financial Services | Singapore |

|

|

EM Topco Limited (Element Materials Technology)4 | 88 | USD’m | 2,543 | 3,195* | Transportation & Industrials5 | UK |

|

|

Global Healthcare Exchange, LLC | 71## | NA6 | NA6 | NA6 | Telecommunications, Media & Technology | US |

|

|

HDFC Bank Limited | <1 | INR’m | 10,999,567 | 8,980,875 | Financial Services | India |

|

|

ICICI Bank Limited | 2 | INR’m | 7,677,520 | 6,125,675 | Financial Services | India |

|

|

Industrial and Commercial Bank of China Limited | 1 | HKD’m | 1,887,947 | 1,736,141 | Financial Services | China |

|

|

Keppel Ltd.7 | 21 | SGD’m | 13,026 | 9,900 | Transportation & Industrials5 | Singapore |

|

|

M+S Pte. Ltd. | 40 | NA8 | NA8 | NA8 | Consumer & Real Estate | Singapore |

|

|

Mandai Park Holdings Pte. Ltd. | 100 | SGD’m | 1,049 | 779 | Consumer & Real Estate | Singapore |

|

|

Manipal Health Enterprises Private Limited | 35 | INR’m | 40,286 | 32,421 | Life Sciences & Agri-Food | India |

|

|

Mapletree Investments Pte Ltd | 100 | SGD’m | 18,979 | 19,908 | Consumer & Real Estate | Singapore |

|

|

Mastercard Incorporated | <1 | USD’m | 445,067 | 342,114 | Financial Services | US |

|

|

Moncler S.p.A. | 4 | EUR’m | 18,721 | 17,162 | Consumer & Real Estate | Italy |

|

|

NSE India Limited | 5 | INR’m | 239,744 | 204,785 | Financial Services | India |

|

|

Olam Group Limited | 52 | SGD’m | 4,268 | 6,033 | Life Sciences & Agri-Food | Singapore |

|

|

Ping An Insurance (Group) Company of China, Ltd. | 2 | HKD’m | 718,593 | 935,745 | Financial Services | China |

|

|

PSA International Pte Ltd | 100 | SGD’m | 15,050 | 14,317 | Transportation & Industrials5 | Singapore |

|

|

SATS Ltd. | 40 | SGD’m | 3,876 | 4,150 | Transportation & Industrials5 | Singapore |

|

|

Schneider Electric India Pvt. Ltd. | 35 | INR’m | 120,961 | 103,806 | Transportation & Industrials5 | India |

|

|

Seatrium Limited9 | 36 | SGD’m | 5,389 | 8,188 | Transportation & Industrials5 | Singapore |

|

|

Sembcorp Industries Ltd | 49 | SGD’m | 9,612 | 7,792 | Transportation & Industrials5 | Singapore |

|

|

Singapore Airlines Limited | 53 | SGD’m | 19,033 | 17,021 | Transportation & Industrials5 | Singapore |

|

|

Singapore Power Limited | 100 | SGD’m | 12,874 | 12,317 | Transportation & Industrials5 | Singapore |

|

|

Singapore Technologies Engineering Ltd | 51 | SGD’m | 12,542 | 11,413 | Transportation & Industrials5 | Singapore |

|

|

Singapore Technologies Telemedia Pte Ltd | 100 | SGD’m | 4,682 | 5,035 | Telecommunications, Media & Technology | Singapore |

|

|

Singapore Telecommunications Limited | 51 | SGD’m | 41,753 | 40,600 | Telecommunications, Media & Technology | Singapore |

|

|

SMRT Corporation Ltd | 100 | SGD’m | 1,010 | 972 | Transportation & Industrials5 | Singapore |

|

|

Standard Chartered PLC | 17 | GBP’m | 17,547 | 17,422 | Financial Services | UK |

|

|

Tencent Holdings Limited | <1 | HKD’m | 2,869,391 | 3,689,755 | Telecommunications, Media & Technology | China |

|

|

Visa Inc. | <1 | USD’m | 565,13710 | 468,28010 | Financial Services | US |

|

|

Zomato Limited | 4 | INR’m | 1,580,674 | 426,563 | Telecommunications, Media & Technology | India |

- For year ended September 2023/2022.

- For year ended December 2023/2022.

- For year ended March 2024/2023.

1 Market Capitalisation or Shareholder Equity: For listed companies, 2024 refers to market value as at 31 March 2024. For unlisted companies, 2024 refers to shareholder equity reported by respective companies based on their annual fillings as at 31 March 2024 or 31 December 2023, in accordance with their respective financial year ends. Similarly for 2023.

2 Percentages rounded to the nearest whole number.

3 AS Watson Holdings Limited was formerly known as A.S. Watson Holdings Limited with name change effective from 22 January 2024.

4 EM Topco Limited is the holding company for Element Materials Technology Group Limited.

5 The Transportation & Industrials sector includes investments in Energy & Resources.

6 Information not disclosed due to confidentiality obligations.

7 Keppel Ltd. was formerly known as Keppel Corporation Limited with name change effective from 1 January 2024.

8 Joint venture with Khazanah Nasional Berhad. Information not disclosed due to confidentiality obligations.

9 Following the combination of Sembcorp Marine Ltd and Keppel Offshore & Marine Ltd on 28 February 2023, Sembcorp Marine Ltd was renamed as Seatrium Limited with effect from 26 April 2023.

10 Based on number of shares of class A common stock on an as-converted basis.

* Restated or reclassified, which includes effects of changes to accounting standards and/or adjustments due to change in basis.

# Held through CLA Real Estate Holdings Pte. Ltd. (“CLA”), a wholly-owned subsidiary of TJ Holdings (III) Pte. Ltd.

## Comprises a 71% stake held through various holding companies.

Temasek’s Credit Profile12 is a snapshot of our credit quality and financial strength, serving as a public marker along with our credit ratings. For these ratios, the lower the percentage, the higher the credit quality.

(as at 31 March)

Total Debt

5% of Net Portfolio Value

- Total Debt

- Net Portfolio Value

Total Debt

18% of Liquid Assets1

- Total Debt

- Liquid Assets

1 Mainly cash and cash equivalents, and sub-20% listed assets.

Interest Expense

6% of Dividend Income

- Interest Expense

- Dividend Income

Interest Expense

1% of Recurring Income1

- Interest Expense

- Recurring Income

1 Divestments, dividend income, income from investments, and interest income.

Total Debt due in One Year

2% of Recurring Income1

- Total Debt due in One Year

- Recurring Income

1 Divestments, dividend income, income from investments, and interest income.

Total Debt due in next 10 Years

15% of Liquidity Balance1

- Total Debt due in next 10 Years

- Liquidity Balance

1 Cash and cash equivalents, and short-term investments.

As an investment company, our divestments, dividends from our portfolio and distributions from funds are used to make investments, fund business expenses, as well as pay interest and principal to bondholders and Euro-commercial Paper holders, taxes to tax authorities, and dividends to our shareholder.

For the year ended 31 March 2024, Temasek made S$33 billion of divestments, which include fund distributions, and earned S$9 billion in dividend income. These amounts formed the bulk of our recurring income.

We aim to build a resilient and forward-looking portfolio. We maintain sufficient access to liquidity to not only serve as a buffer against shocks in this uncertain environment, but also to allow us to take advantage of investment opportunities. Our portfolio includes high-quality assets that provide us with strong and stable liquidity. We also maintain the discipline of regular divestments to generate liquidity.

We are rated Aaa/AAA by Moody’s Investors Service and S&P Global Ratings respectively13. Ratings are an outcome of credit rating agencies’ independent assessment of Temasek’s business and financial position in accordance with their respective methodologies.

Key Credit Parameters (in S$ billion)

| For year ended 31 March | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Divestments | 26 | 39 | 37 | 27 | 33 |

| Dividend income | 11.9 | 8.4 | 9.4 | 11.1 | 9.0 |

| Income from investments | 0.8 | 0.7 | 1.0 | 0.9 | 0.9 |

| Interest income | 0.7 | 0.1 | 0.1 | 0.6 | 1.4 |

| Interest expense1 | 0.4 | 0.4 | 0.5 | 0.5 | 0.5 |

| Net portfolio value | 306 | 381 | 403 | 382 | 389 |

| Liquid assets2 | 112.4 | 143.1 | 113.6 | 104.5 | 113.0 |

| Liquidity balance3 | 47.1 | 50.8 | 38.4 | 43.7 | 61.8 |

| Total debt1,4 | 13.9 | 17.6 | 22.0 | 21.7 | 20.9 |

1 From the year ended 31 March 2020, the applicable accounting standard (IFRS 16: Leases) has required us to record our leases, comprising mainly office rental, on our balance sheet. This means that our lease liabilities and interest expense on lease liabilities are included as part of total debt and interest expense respectively. The credit ratios from the year ended 31 March 2020 reflect this change in accounting standards.

2 Mainly cash and cash equivalents, and sub-20% listed assets.

3 Cash and cash equivalents, and short-term investments.

4 As at 31 March 2024, we had S$20.2 billion of Temasek Bonds and S$0.5 billion of Euro-commercial Paper (ECP) outstanding, in equivalent Singapore dollar value. The weighted average maturity for Temasek Bonds was over 18 years, and above four months for our ECP. All Temasek Bonds issued to date have been rated Aaa by Moody’s Investors Service (Moody’s) and/or AAA by S&P Global Ratings (S&P). Our ECP Programme has short-term ratings of P-1/A-1+ by Moody’s and S&P respectively.

There are inherent risks whenever we invest, divest, or hold our assets, and wherever we operate.

While we adopt a long-term view of our portfolio, we invest across different time horizons. We have the flexibility to take concentrated positions and invest across all stages of the business life cycle, from early-stage to mature, and unlisted to listed assets. We do not have specific targets for investing by asset class, country, sector, or single name.

Our long investment horizon means we have a portfolio of predominantly equities which is expected to deliver higher risk-adjusted returns over the long term. Our stable funding base allows us to invest and benefit from companies with high growth potential through listed and unlisted assets (including private equity funds).

Consequently, given the high equity exposure, our portfolio is expected to have higher volatility of returns, with a greater risk of negative returns in any one year.

Our investment approach is to ride out short-term market volatility and focus on generating sustainable returns over the long term.

Given the expected volatility, we manage our leverage and liquidity prudently for resilience and investment flexibility, even in times of extreme stress.

Our investment posture is coupled with a culture of risk ownership throughout the organisation. Our risk-sharing compensation philosophy puts the institution above the individual, emphasises the long term over the short term, and aligns the interests of our staff with those of our shareholder.

We have no tolerance for risks that could damage the reputation and credibility of Temasek.

Our Organisational Risk Management Framework includes Risk Return Appetite Statements which set out various levels of risks tolerance, from reputational risk to liquidity risk, and risk of sustained loss of overall portfolio value over prolonged periods.

Organisational Risk Management Framework

Risk Return Appetite Statements

We have no tolerance for risks that could damage Temasek’s reputation and credibility

- Temasek rigorously identifies potential sources of reputational risk and how each type of reputation risk is to be managed

We focus on performance over the long term

- We target a long-term portfolio return that exceeds our risk-adjusted cost of capital

- We are prepared to accept fluctuations in annual reported results provided we are compensated by superior longer-term returns and it does not affect our ability to survive

We have flexibility to take concentrated positions

- Where good investment opportunities allow for superior long-term performance, Temasek has the flexibility to take portfolio concentrations in specific sectors, geographies, themes, or individual assets

- We adopt a disciplined approach to investing, with end-to-end assessment frameworks and processes for each asset class

- For direct equity investments this includes developing a deep understanding of each investment in order to determine the intrinsic value for investment, divestment, and hold decisions

We maintain a resilient balance sheet

- We manage leverage and liquidity to ensure resilience and flexibility even in times of extreme stress

We evaluate the potential for sustained loss of overall portfolio value over prolonged periods, and use different scenarios to test our resilience

Risk Pillars

Investment Risk1

Liquidity & Leverage Risk

Portfolio Value Risk

Operational Risk

Cybersecurity Risk

Legal & Regulatory Risk

Macro and Geopolitical Risk

1 Includes Foreign Exchange Risk and Environmental, Social, and Governance Risk.

Risk Governance

There are various risk pillars by which we assess risks across a wide spectrum of domains. These risk pillars are supported by specialised teams, comprising members from different functions, which report to senior management for general oversight. We embed risk management in our systems and processes. These include our approval authority delegation, company policies, standard operating procedures, and risk reporting to our Board and Board Risk & Sustainability Committee.

Investment Risk

All new investment proposals are subject to a due diligence process commensurate with the nature of the investment to be made. This is intended to validate business theses and examine material risks. The exact scope of the required pre-investment analysis will be determined based on the specific risk profile being considered. Pre-investment analysis is done by our deal origination teams whose expertise is supplemented by internal experts or external professionals who perform additional due diligence in specialised areas such as legal, tax, and climate risks.

When we invest in companies, we conduct a bottom-up fundamental valuation analysis and due diligence. We also use an appropriate risk-adjusted cost of capital (RACOC) to determine a best estimate of company valuation. Our analysis enables us to estimate a fair value for the company. We also estimate stress case valuations to help us gauge the degree of variability in potential future returns under different assumptions.

We will compare our reasonable estimate of fair value with current market valuation to determine if an investment makes sense at the proposed price, and if it provides a margin of safety to our RACOC, including an estimated cost of carbon emissions.

The discount rate used in the valuation process will be a weighted average of the company’s cost of debt and equity capital. We utilise the capital asset pricing model to derive an appropriate cost of equity. This takes into account leverage, the type of industry, and the countries of operation. Investments in riskier sectors or markets will have higher costs of capital. We also add an illiquidity risk premium for unlisted investments and a venture risk premium for early-stage investments to account for their respective risks.

We use individual companies’ RACOC to compare the relative attractiveness between investment opportunities. We may dial up or down the required spread over RACOC as a tool to tighten or loosen our investment risk posture.

Depending on the external outlook and our investment stance, we may choose to invest in opportunities with positive expected returns, which are below their respective individual RACOC. We also deploy excess liquidity in short-term liquid investments where the expected returns may be lower than our cost of capital.

All prospective investments must be reviewed and approved by our investment committee.

Investment proposals made to the investment committee are typically submitted by both market and sector teams who provide geographic and industry expertise. Depending on the size or risk significance, these proposals may be escalated to our Board Executive Committee or Board for a final decision.

Post-investment monitoring is performed by the investment teams on a continuous basis, and formally by senior management at quarterly review meetings chaired by the Deputy CEO. They assess if the investment is performing to our expectations and whether any action should be taken.

Foreign Exchange Risk

Our projected risk-adjusted return for each investment proposal takes into account any anticipated foreign exchange (FX) movements against the Singapore dollar.

We also selectively hedge FX exposures from confirmed nearer-term cash flow and expected divestments within our forecast period.

Environmental, Social, and Governance Risk

Our investments are evaluated on the basis of our Environmental, Social, and Governance (ESG) framework, which is integrated within the investment process. This framework requires the analysis of material ESG considerations, with an emphasis on climate-related risks.

As part of our analysis, we apply an internal carbon price of US$6514 per tonne of carbon dioxide equivalent (tCO2e)15. This provides an additional consideration to our assessment of the long-term climate resiliency and our returns expectations for each investment.

We are also strengthening our analytic capabilities to enhance our pre-investment due diligence and post-investment engagements to address material nature-related risks.

We piloted a set of baseline expectations in social areas such as human rights and labour practices; diversity, equity, and inclusion; talent management; product quality and safety; data privacy and security; and supply chain responsibility. To manage and mitigate such risks, we conduct deeper due diligence in cases where potential exposure to social risk is identified.

Our Board Risk & Sustainability Committee (RSC) was established in January 2022 to, amongst other things, enhance the focus on opportunities and risks arising from sustainability trends, including climate change, and other financial, reputational, operational, and cyber risks.

Liquidity & Leverage Risk

We manage our leverage, liquidity, and balance sheet prudently for resilience and flexibility. We maintain a high level of liquidity in our portfolio and manage our liquidity risk by ensuring that our primary recurring sources of cash flows are able to cover our non-discretionary uses of cash, such as operating expenses, taxes, and interest to bondholders.

Our recurring income includes divestments, dividends from portfolio companies, and distributions from funds.

Our liquidity is supported primarily by our recurring income, supplemented by proceeds from any debt issuances via Temasek Bonds and Euro-commercial Paper, as well as bank borrowings. Total leverage is restricted by an overall debt limit set by our Board. The debt limit takes into account our portfolio value, shareholder funds, forecast cash flow, and credit profile. We proactively plan for a well-distributed debt maturity profile, avoiding large refinancing risk in any one year.

In addition to maintaining the discipline of regular divestments to generate liquidity, the construction of our portfolio enables us to access liquidity relatively quickly in times of stress. As at 31 March 2024, our liquid and sub-20% listed assets alone were about five times our debt outstanding. In the highly unlikely extreme scenario where we have no other cash inflows, aside from using our liquidity balance, divesting a small part of our liquid and sub-20% listed assets would be sufficient to cover the total debt outstanding in under two weeks16.

As a policy, Temasek does not provide any financial guarantees for the obligations of our portfolio companies.

Portfolio Value Risk

We track and manage risks proactively, through economic and market cycles, including specific risks at the asset level.

We assess the sustained impact of multiple risk scenarios on the intrinsic value of our investments. The aggregate of these changes provides an estimate of the portfolio level variation in present value, future cash flows, and income in each scenario.

As illustrated in the diagram below, Fundamental Earnings Impact is our estimate of sustained loss. This is different from Trough Impact, which includes mark to market effects due to short-term increases in risk aversion. In a stress event, our largely equity portfolio will likely be adversely affected by market volatility reflecting increased short-term risk aversion. However, markets typically recover from the trough and normalise after the stress event is over. Over time, we expect our portfolio value to recover towards the previous growth rate, but from a lower starting point.

We do not manage our portfolio to short-term mark to market changes.

Illustration of Fundamental Earnings Impact

- Base Case

- Stress Scenario

Based on our assessments of any likely sustained loss, consistent with our intrinsic value discipline, we may manage the risks as follows:

- Divest, hold, or protect the individual investment impacted;

- Change the portfolio composition for the long run;

- Take actions to protect the portfolio, for example, by entering into tactical single stock, index or rates hedges.

12-months Returns Simulation

While we expect volatility consistent with a largely equities portfolio, we manage our portfolio to deliver sustainable returns over the long term.

For our current portfolio mix, our Monte Carlo simulations based on recent market conditions show a five-in-six chance that one-year forward portfolio returns may range from -10% to +15%. Our annual returns ranged from -30% to +43% over the past 20 years.

Narrower curves in the chart below mean less volatility compared, for instance, to the flatter curves of the 2008/09 Global Financial Crisis (GFC) years. A wider simulated range means a more volatile outlook.

(as at 31 March)

Simulation of 12-month Forward Portfolio Returns

1 Based on Monte Carlo simulation for 12-month forward portfolio returns distribution, assuming no change in market conditions or portfolio mix.

2 Total Shareholder Return.

3 Periods of low market volatility.

4 Periods of medium market volatility.

5 Periods of high market volatility.

(as at 31 March)

Volatility of Returns (%)

- Simulated returns1 in a period of low market volatility

- Simulated returns1 in a period of medium market volatility

- Simulated returns1 in a period of high market volatility

- Actual Total Shareholder Return a year later

1 Based on Monte Carlo simulation for 12-month forward portfolio returns distribution, assuming no change in market conditions or portfolio mix.

The range of possible returns from the simulation is dependent on the prevailing volatility and correlation conditions of asset markets. When prevailing volatility is high, such as at the onset of the COVID-19 pandemic or during the GFC years, the wider range of one-year simulated forward returns signals greater probability of larger gains and losses. When volatility is low, as at present, simulated forward returns fall within a narrower range. However, history shows that periods of lower volatility may be followed by sudden dislocations. We therefore complement these estimates based on current conditions with the scenario stress tests process described above.

Operational Risk

We are committed to continuously improving the way we manage business continuity risks. Our contingency management framework ensures business continuity and covers incidents arising from safety, physical security, and other threats. The framework also takes into account the potential impact of emerging risks, such as physical threats and health situations around the world.

We have institutionalised a risk incident reporting process which encourages staff to proactively report gaps, perform root cause analysis, and adopt appropriate remediating measures for all reported risk incidents. This contributes to a work environment with a focus on excellence and helps build a healthy risk management culture in Temasek.

In response to growing physical security threats, we provide regular training to relevant stakeholders to adequately equip them with response techniques for emergency situations. For instance, Evacuation Wardens receive occupational first aid training, while our Business Continuity Planning Coordinators and front-line Emergency Response Team undergo emergency response training. Additionally, we have established multiple communication channels to ensure effective information dissemination. This proactive approach enables us to respond promptly and confidently in times of emergencies.

In addition to the training, we regularly conduct response exercises simulating critical infrastructure failures, and scenario-based tabletop exercises with key stakeholders to ensure that our contingency and disaster recovery plans remain effective, relevant, and adequate. We constantly work on improving our capabilities to ensure that our staff and visitors remain safe, and that critical business functions can resume in a timely manner.

For crisis management, the primary focus typically revolves around strategies and swift decision-making. While these elements are crucial, the mental well-being of our staff is equally paramount. As such, we have integrated our Care Supporters network into our crisis management processes. This significantly enhances our ability to manage crisis response and recovery efforts effectively. To strengthen psychological resilience amongst staff, more than 70% of our staff have been trained and equipped with basic psychological support skills.

Cybersecurity Risk

Given the evolving cybersecurity landscape, we regularly monitor and track cyber risks and continuously enhance our cybersecurity defence and resilience. We continually assess and perform regular testing of our environment to ensure our cybersecurity controls are effective, and are committed to enabling secure deployments of applications and technologies that support business needs. Most recently, we established an Artificial Intelligence (AI) governance framework to enable secure AI deployment across the firm. In addition, we conduct simulation exercises and update our cyber response plans on a regular basis to ensure continued relevance, familiarity, and effectiveness.

We engage our portfolio companies, together with our Temasek Operating System partners, on an ongoing basis to champion cybersecurity best practices and to elevate our respective cyber defence and resilience capabilities. This year, we also introduced a Board-level Cyber Risk Governance Guideline to support board oversight of cyber governance and standards in our portfolio companies.

Our cybersecurity team, supported by expertise from our cybersecurity platform companies, assesses the cybersecurity health of potential investee companies as part of the investment due diligence process. Their assessment is based on four areas: key data assets; regulatory requirements and data privacy; cybersecurity policy and governance; and assessment and incidents. A comprehensive cybersecurity scan on potential investee companies may also be conducted.

Legal & Regulatory Risk

We comply with all obligations under Singapore laws and regulations, including those arising from international treaties and UN sanctions, as well as the laws and regulations of jurisdictions where we have investments or operations.

Our global footprint, coupled with a fast and ever-evolving legal and regulatory environment and increasing enforcement and oversight by authorities, reinforces the importance of robust transactional processes and compliance programmes. We continue to build expertise across novel and developing areas that we are involved in to ensure that we are able to identify and manage legal, regulatory, and compliance risks appropriately.

Our Legal & Regulatory (L&R) department ensures that policies, processes, and systems are appropriately designed and implemented, consistent with applicable laws and aligned with Board directives to advance the firm’s objectives while managing risks and safeguarding its interest. For example, we have implemented policies and control processes to address financial crime such as bribery and corruption, and sanctions violations; to ensure compliance with foreign direct investment, merger control, and export control regimes; and to manage legal and regulatory risks relating to the trading of derivatives. We continuously monitor regulatory developments to ensure that our policies, procedures, and monitoring systems reflect these changes.

We encourage and facilitate the development of a sound corporate culture that incentivises good staff behaviour. High ethical standards and compliance with applicable laws and regulations are expected in the pursuit of our business interests. Specific attention is directed at governance, incentive systems, and training.

At the core of this is our Temasek Code of Ethics and Conduct (T-Code) and its related policies that guide our Board directors and staff in their daily dealings and conduct. With integrity as the key overarching principle, T-Code policies cover areas such as anti-bribery, whistle-blowing, management of confidential information, and prohibition against insider trading. All staff also undergo mandatory training in anti-bribery and corruption, anti-harassment and discrimination, as well as the prevention of insider trading. Our annual staff bonus plans include T-Code compliance requirements.

Macro and Geopolitical Risk

Over the last decade, besides the ever-changing macroeconomic landscape, we have seen heightened geopolitical tensions arising from events such as war and the pandemic, as well as great power rivalry.

Our views around the global economy help to guide Temasek’s investment stance and our overall deployment pace. We also recognise that there has been a renewed and urgent focus on national security (encompassing economic security and competition), resiliency including energy and commodity sufficiency, data ownership, techno-nationalism in sectors such as biotechnology, and the use of subsidies, to name a few pressing issues. The presumptive gains from the globalisation of trade, investment, and technology are subject to ever-greater scrutiny.

To stay ahead of these developments, our International Policy and Governance teams — located in Beijing, Brussels, Singapore, and Washington, DC — actively monitor geopolitical risks and anticipate policy developments in our key markets that could impact our activities.

Through our engagement with thought leaders and authorities, we exchange views so as to promote better outcomes for all in the design and implementation of policy. In particular, we aim to promote a better understanding of how we operate based on commercial principles, and independent of government interference and support. For example, we had supported the International Monetary Fund initiative to frame the Santiago Principles for sovereign investments back in 2008. We advocate good governance and uphold these principles.